South Korea Joins Asian Equity Party

On December 6, we pointed out a potential “bear flag” in the chart of South Korea’s main stock average, the KOSPI Index. As the name implies, this is a bearish pattern that typically results in lower prices. In this case, the bear flag was about 6 weeks in the making and therefore most relevant on a shorter-term duration. This is what we wrote regarding the risk suggested by the bear flag pattern:

Should the bear flag implications pan out, the first target would be a retest of the October lows just below 1900. An undercut of that area would not be a surprise and the Index would quickly hit the up trendline connecting the 2010, 2011 and 2013 lows, currently around 1870. That may provide a springboard for a better bounce.

Well, it certainly isn’t always the case, but sometimes prices actually do what they’re supposed to do. In this instance, the prior day’s close in the KOSPI marked THE top in the short-term as the potential risk suggested by the bear flag began to manifest itself immediately. Just 6 days later, the KOSPI had sold off by nearly 5%, bottoming right at the first target at 1899. After a few days worth of a bounce, the KOSPI did undercut the October lows and approached the upward sloping long-term trendline that we mentioned. After bouncing again for a few days, the index returned to test those lows, bottoming in early January right on that trendline around 1876. Subsequently, the “springboard” indeed engaged.

In the 3 months since, the KOSPI has been on fire, gaining some 14% over that time. And importantly, last week the index broke out above its highs of last August to a nearly 4-year high.

As the chart illustrates, the breakout level in the mid to upper-2000′s had served as resistance since 2012. Furthermore, the KOSPI’s high in 2007 was formed right at the same level. therefore, this was a significant hurdle to overcome. The obvious catch is that the 2011 all-time highs await about 4% above current levels. Naturally, that should serve as some stiff resistance, particularly if the index should rally immediately up to that level. After closing higher for 12 of 13 days (the one loss was -0.019%) and 13 of 15 weeks, the index could use a breather. It is doubtful that the KOSPI would be successful in breaking its all-time highs without one. Therefore, some consolidation perhaps up near those highs could allow the index to join several of its Asian counterparts in record territory.

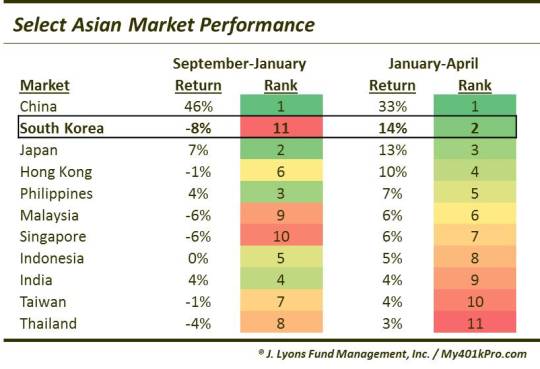

Speaking of other Asian markets, the table below reveals just how dramatic the KOSPI’s reversal of fortune has been in the months since our “bear flag” post.

While other Asian markets were breaking out in the middle to late 2014 (e.g., China, Japan, India), South Korea was bringing up the rear in relative performance. Since bottoming in January, however, its fortunes have changed. Only the China Shanghai Composite is up by more than the KOSPI over the past 3 months (at +33%, how could it not be?). The KOSPI has even surpassed some of the smaller Asian markets (e.g., Indonesia and the Philippines) whose breakouts we highlighted earlier in the year.

With several Asian equity markets exhibiting high-profile rallies – China, Hong Kong and Japan, in particular – the move in South Korean stocks the past 3 months has flown under the radar. However, the Korean KOSPI index was able to achieve a significant milestone last week in breaking out to near 4-year highs. And though the index may be a little overheated in the short-term, its all-time highs set in 2011 are within striking distance. Once the China equity fervor dies down a bit, more eyes, and money, may turn to South Korea. Such a turn may be enhanced or expedited given perhaps some relative monetary leeway on the part of the Bank of Korea should they look at the party in Asian equities and say, “we want in”.

_____________

“Seoul” photo by Clint Sharp.

More from Dana Lyons, JLFMI and My401kPro.

The commentary included in this blog is provided for informational purposes only. It does not constitute a recommendation to invest in any specific investment product or service. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.