European Investors (Over?-)Prepared For Volatility

We were desperately hoping to make it through this “crisis” season without a single mention of the word Greece. Alas, it was not to be as we observed a developing situation that piqued our interest. Rest assured that the intent of this post is not to add our own unqualified guess as to the outcome of the Greek charade – or the market’s reaction thereof. Well, perhaps the observations here do pertain the financial markets’ ultimate handling of the situation. However, our intent is merely to point out present circumstances rather than to opine on forthcoming developments. So what was so interesting that it persuaded us to forego our pledge to avoid the “G-word”?

Much of the talk in the capital markets surrounding the Greece situation has been related to the question of “how much event risk is priced into the markets?” There is no shortage of opinions on the matter. There are plenty of folks arguing that investors are too complacent regarding the situation. Conversely, there are those that claim the Greece worry is overdone. So which is it? Well, the subject of our Chart Of The Day would appear to possibly favor the latter camp, i.e., investors are too worried about the situation.

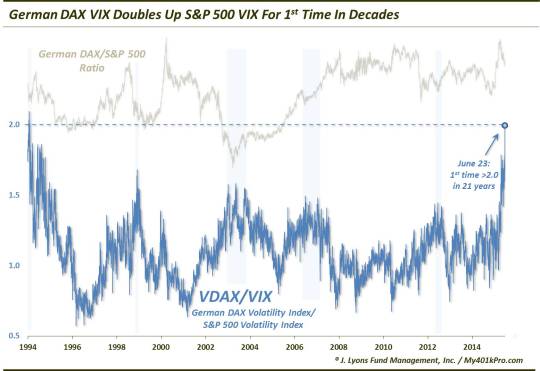

Why do we say that? Consider this statistic related to the VDAX, the Volatility Index on the German DAX Stock Index. Relative to the S&P 500 Volatility Index, or VIX, the VDAX closed today at a ratio of over 2:1, i.e., the VDAX was twice as high as the VIX. How unusual is this reading? The last time the VDAX doubled up the VIX was over 2 decades ago, not long after the VDAX’s inception.

I know you’re probably thinking “duh, the DAX Volatility Index should be higher than the S&P 500 Volatility Index given the Greek circumstances”. No argument here. However, should it be this much higher?

The VDAX has never priced in this much volatility versus the VIX, save for some questionable readings in early 1994. And during the past 2 decades, Europe has been through its share of crises and hardships. Yet, the VDAX/VIX ratio never approached 2.0. Sure, an ugly outcome to the Greek mess will no doubt inflict some considerable damage on the German and European equity markets. However, it seems far-fetched to think that the U.S. markets would be completely immune to such an outcome. And yet, that is precisely what the VIX seems to be pricing in, having closed at a year-to-date low today. On the other hand, the VDAX is pushing multi-year highs.

You may also be thinking, “yeah, but on an absolute basis, the VDAX isn’t really that high”. We would probably take exception to that argument. While it is true that the VDAX is well below prior historical peaks, let’s put the move into context. As of last week, the German DAX was down about 10% from its April high. However, this was following an epic breakout to new high ground in January and a gain of as much as 30% afterward. Again, the DAX and other European markets have seen worse than that, even in the past few years. Yet, the VDAX is near its highest levels in nearly 3 years. Considering this tepid, post-breakout retracement in the DAX, the rise in the VDAX seems a bit much.

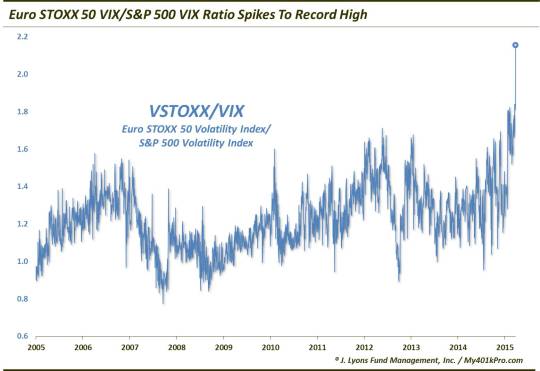

By the way, it isn’t just the German equity market showing skewed relative volatility expectations. The broad Euro STOXX 50 Volatility Index, or VSTOXX, has also been spiking versus the S&P 500 VIX. And while the historical data on the VSTOXX only goes back just over 10 years, the current readings are head-&-shoulders above anything we’ve seen during that period.

Lastly, what is the significance of the spike in the VDAX versus the VIX? Is it merely a fluke given the unique circumstances in Europe? Or is there something applicable, if not actionable, based on previous historical spikes in the VDAX/VIX ratio?

Well, as we mentioned, there has been just one other instance when the the ratio rose above 2.0. That was at the beginning of 1994, not too long after the inception of the VDAX. And while we hate to dismiss data points arbitrarily, the readings back then just seem a little odd given the circumstances at the time. For one, it may have had something to do with the newness of the VDAX market. Secondly, the stock markets at the time, both in the U.S. and in Germany, were going through a historically flat, involatile period. And while the exceptionally low VIX at the time certainly would have contributed to a rise in the VDAX/VIX ratio, an elevated VDAX does not make a lot of sense given the investing climate then.

Therefore, we’ll have to loosen the parameters a touch on our VDAX/VIX “spike” readings in order to observe whether or not there has been a historical tendency following such readings, whatever it may be. For this, we merely used the eyeball test, rather than the type of statistical analysis we often do. Thus, from observing the chart, there have been arguably 4 other periods that saw a spike (to approximately the 1.5 level) in the VDAX/VIX ratio. Each of these periods (shaded in blue on the first chart) saw a subsequent bottoming in the DAX/S&P 500 ratio (top line on the first chart) followed by a rally of a decent magnitude in the ratio. In other words, following substantial spikes in the VDAX/VIX ratio, the German DAX went on to a period of significant outperformance versus the S&P 500. It didn’t always occur immediately but it did happen after those prior spikes. (The only time it did not transpire was following the sketchy 1994 readings.)

So what’s the point? Amid the Greece situation, it seems from the pricing in volatility indexes between Europe and the U.S. that investors across the pond are expecting a whole lot more volatility than investors are in the U.S. – in fact, a record degree more. And while we don’t claim to have any better gauge on the outcome of this mess than anyone else, this record discrepancy would appear to quite possibly represent an under-pricing of volatility, or risk, in the U.S. or an over-pricing of volatility, or risk, in Europe – or some combination of the two. Based on prior, albeit less significant, spikes in the VDAX/VIX ratio, that combination may indeed be rewarding eventually for European stock investors at the expense of U.S. investors. While that remains to be seen, there is no doubt that European investors are far more prepared for imminent volatility than U.S. investors – perhaps to a fault.

________

More from Dana Lyons, JLFMI and My401kPro.

The commentary included in this blog is provided for informational purposes only. It does not constitute a recommendation to invest in any specific investment product or service. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.