Investor Complacency Is Smashing Records

Near-term volatility expectations are currently on a stretch of unprecedentedly low levels.

About a month ago, we began to take note of investor complacency creeping into the stock market. At the time, the major averages had recently broken out to all-time highs amidst strong breadth readings and favorable seasonality. Thus, such complacency, or optimism, was arguably warranted. As such, our take was that the positive price action and participation was certainly enough to override the budding excessive bullishness. We have seen that, in such circumstances, sentiment extremes can persist for an extended period of time before any negative consequences unfold. Indeed, the markets have continued to creep higher ever since, along with investors’ optimism. At this point, however, sentiment is getting to the point where it is a legitimate red flag, in our view. In fact, by one measure, the market has never witnessed a stretch of such investor complacency.

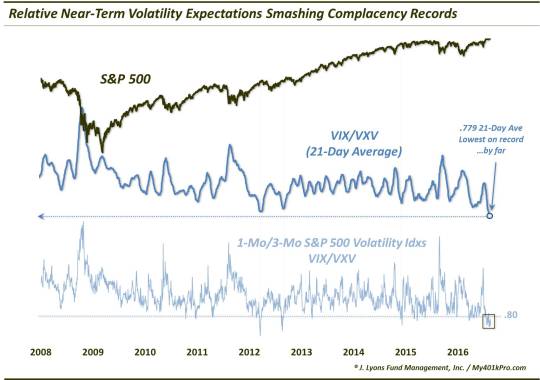

The measure to which we are referring is the same as that noted in the late July post above, and pertains to investors’ volatility expectations. As we wrote:

One way of using volatility to measure the extent of investor nervousness is by comparing near-term volatility expectations versus those farther out. For example, the VIX is actually the 1-month S&P 500 volatility index. Meanwhile, the VXV is the 3-month volatility index. Typically, the VIX will be lower than the VXV as there is less time in the near-term for volatility rises to occur. When investors get especially nervous (usually during a selloff), near-term volatility expectations can actually rise above those farther out, i.e., the VIX/VXV ratio rises above 1.00. Conversely, during times of complacency, the VIX will drop to relatively low levels versus the VXV; historically, under 0.80 may be considered complacent.

At the time, the VIX/VXV ratio had actually dropped below 0.78, a level it had only reached on 14 prior days since the inception of the VXV in late 2007. As we noted, such complacency can persist for a short while, especially amidst positive developments elsewhere in the equity markets. However, at this point complacency has extended beyond any historical precedent. Specifically, while just 14 days in the past 9 years (prior to July) had ever seen VIX/VXV readings below 0.78, this week saw the 21-day average (approximately 1-month) drop below that level.

Obviously, the market can almost literally do anything – there are no rules. Thus, it may continue to accommodate investors’ lack of volatility expectations for a while longer. However, we are already in uncharted waters. The only time the 1-month average VIX/VXV dropped even below 0.80 was in March 2012. FWIW, the ratio remained below 0.80 for the next 11 days. Meanwhile, the S&P 500 gained a maximum of just 1% as it meandered sideways for the next 5 weeks before getting clipped for nearly 10% over the subsequent month.

Again, we don’t have a script for what will play out here (there is no script for a VIX/VXV ratio this low). The 2012 outcome is just one potential template. There are still enough positives in the equity market in the near-term that could certainly keep the stock market propped up for the time being. And we do not have any major signals at this point to suggest bailing out of stocks en masse.

However, we do consider this data point to be one that warrants our attention. Therefore, we would perhaps raise the proverbial “DefCon” from 1 to 2. While that may not mean taking much defensive action yet, it should at least up one’s readiness, whether that means tightening stops, looking for hedges or just plain being more prepared.

At the very least, we would recommend investors not get lulled to sleep by the present calm in the markets.

_________

More from Dana Lyons, JLFMI and My401kPro.

The commentary included in this blog is provided for informational purposes only. It does not constitute a recommendation to invest in any specific investment product or service. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.