Options Market: Too Fear Too Fast?

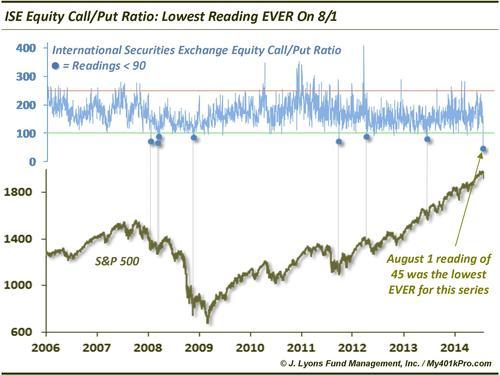

To say that readings in the equity options market on Friday were extraordinary would be a gross understatement. They were downright historic. To wit, our Chart Of The Day: the International Securities Exchange Equity Call/Put Ratio (similar behavior was observed in the CBOE options market as well):

The ISE presents its options ratio opposite of most exchanges, i.e., with the call volume as the numerator. Thus, a low ISE Equity Call/Put Ratio signifies a low level of call activity relative to puts. On Friday, August 1, the ISE Equity Call/Put Ratio recorded its lowest reading in history, as in EVER (data starts in 2006).

Normally these extreme readings occur in a capitulatory phase after a prolonged bout of selling in the market, not 6 days removed from 52-week high. For instance, there had been exactly 7 other readings below 90 before Friday. 3 of them came in early 2008 following heavy selling in January and March, 1 near the low in November 2008, another near the low in September 2011 and 1 more at the low of the pullback in June 2013. The only instance anywhere similar to the current case occurred in April 2012 after a 9-day selloff from a 52-week high that saw minor losses on par with the present. After that occurrence, the market bounced for a few weeks before moving to new lows as selling persisted for about 5 more weeks.

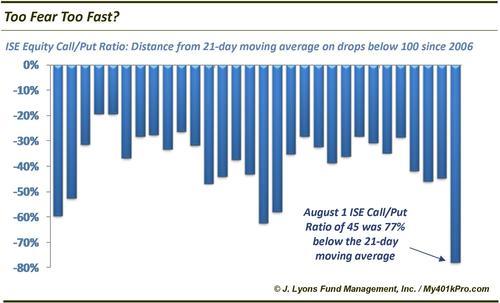

The chart below further illustrates the abnormal behavior in the ISE Equity Call/Put Ratio dropping so low so quickly. It shows the distance from the 21-day moving average during all daily readings in the ISE Equity Call/Put Ratio under 100 since 2006.

On Friday, the ratio dropped 77% below its 21-day moving average. Typically on such days, the spread was about half that, indicating that the 21-day moving average had already dropped considerably before the extreme low daily reading.

To what can this rapid decline in the Call/Put Ratio be attributed? We can’t know for sure but we have one theory: Twitter. The speed of dissemination of both market information and psychology has been increased exponentially by the introduction and popularity of Twitter, and to a lesser extent other social media outlets. This is particularly so as it pertains to the dissemination of analysis by “smart money” sources that, in the past, were not as accessible real-time – if at all. While we don’t believe the medium will have a material effect on long-term market cycles, we can envision an acceleration of cycles in the short-term. This may be what is occurring.

While we see major problems with the stock market over the intermediate and even long-term, perhaps traders have adopted too much fear too fast. This development could allow for a short-term bounce.