What Do Falling Corporate Profits Mean With Stocks Near Their Highs?

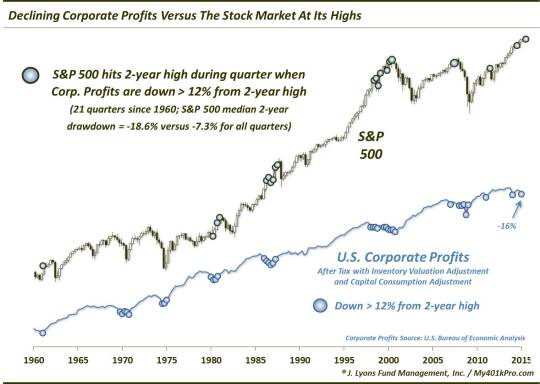

If you’ve followed this blog for awhile, you may have noticed that we don’t cover fundamental or economic data too often. That is for a good reason: we don’t use it, at all. Occasionally, however, a data point will cross the radar that piques our interest for whatever reason. So it is with the current state of U.S. Corporate Profits. The U.S. Bureau of Economic Analysis released the latest data today revealing that Corporate Profits (after Tax with Inventory Valuation Adjustment and Capital Consumption Adjustment) were down 9% for the 1st quarter and are now down 16% from their peak in the 3rd quarter of 2013.

Perhaps we don’t run in the right circles but we haven’t heard much regarding the significance of this trend on the stock market, which continues to trade near its all-time highs. Perhaps that’s a good thing considering we’ve found scant profitable uses for fundamental data in our investment approach (which is why we don’t use it). So we decided to take a look at it ourselves to see what effect similar historical precedents, assuming there were any, may have had on the stock market. This is what we looked for:

- Quarters when Corporate Profits were down at least 12% from their 2-year high, and

- the S&P 500 made a 2-year high at some point within the same quarter.

As it turns out, there have been 21 quarters meeting that criteria since 1960.

Many of the occurrences came in clusters in 1980, 1986-1987 and 1998-2000. There were also single occurrences in 1961, 2007, 2011 and the 1st quarter of last year. Without going into great depth of analysis, one can tell by the inauspicious dates that these circumstances have not worked out well in the past. The stock market may not have rolled over immediately in every occasion (e.g., 1986, 1998, 2014), but it usually ended up paying the piper.

Specifically, the average drawdown over the 2 years following these quarters was -18.6%. This compares with an average 2-year drawdown of -7.3% following all quarters since 1960.

We don’t follow economic and fundamental data too often since we’ve never found it very helpful in our investment decision-making process. At times, however, a certain data series will garner our attention. Often times, as is the case with Corporate Profits presently, it grabs our attention because it is receiving very little attention elsewhere. From just a cursory look at the current trend of falling Corporate Profits, however, it would appear to be a potential negative influence on the stock market that is trading near its all-time highs – if not immediately, then eventually.

________

More from Dana Lyons, JLFMI and My401kPro.

The commentary included in this blog is provided for informational purposes only. It does not constitute a recommendation to invest in any specific investment product or service. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.