Stock Options Traders Easily Spooked

Equity put/call ratios have spiked – despite an unprecedentedly small loss in the averages.

One interesting development related to the stock market currently pertains to sentiment. Namely, investor sentiment has soured considerably over the past month, despite rather modest losses in most of the major averages. This includes various surveys as well as real money sentiment measures. One real money example comes from the options market where put activity has soared relative to calls.

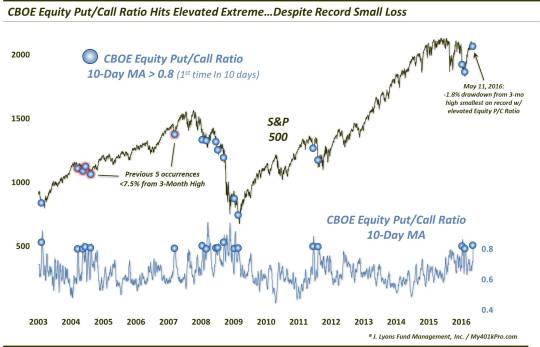

Specifically, the CBOE Equity Put/Call Ratio (CPCE) measures put volume in equities on the exchange relative to equity call volume. While some of the activity is part of more complicated options strategies, for the most part elevated put volume relative to calls reflects increased hedging and heightened fear on the part of traders. And when the CPCE ratio is elevated to an extreme, it can, at times, indicate a contrarian buy signal. That is, traders have become too bearish and too heavily hedged that the market is susceptible to a bounce. Normally, this occurs following significant weakness in the market.

Using a 10-day moving average of the CPCE can smooth out noise in the indicator. On this basis, at over 0.8 puts to calls, the CPCE is presently at an extremely high level, from a historical context. Since 2003, there have been just 17 prior occasions in which the 10-day CPCE rose above 0.8 for the first time in at least 10 days.

The odd thing about our current circumstances is that there has been scant weakness in the market outside of select sectors. Consider the following.

- Of the 17 prior instances since 2003 that saw the 10-day CPCE rise above 0.8 for the first time in at least 10 days, the median return in the S&P 500 over those 10 days was -3.8%. As of May 11, the 10-day return was -1.46%. Only the events on 6/14/04 and 1/13/09 saw milder performance – fractional gains, in fact.

- Of the 17, the median distance of the S&P 500 from its 52-week high was -13.3%. As of May 11, the drawdown was just -3.1%, 2nd smallest to 6/14/04.

-

Of the 17, the median distance of the S&P 500 from its 3-month high was -9.4%. As of May 11, the drawdown was just -1.8%, the smallest drawdown of any of the events.

So, as one can see, our present circumstances are a bit unusual given the elevated CPCE. What does this mean? Instinctively, we would lean toward this being bullish for stocks, on the margin. The suggestion is that traders appear to be disproportionately nervous – and hedged – given the mild losses. The historical evidence may somewhat back up that instinct.

While the sample size is small, consider the S&P 500′s performance following the events with some of the milder losses in the S&P 500. Specifically, here are the results after the 5 prior readings that occurred with the S&P 500 down less than 7.5% from its 3-month high (FYI, 4 occurred in 2004 and the other on 3/13/07).

The median returns, while not out-sized, were consistently positive, with very little in the way of drawdowns. Contrast that with the 12 occurrences when the S&P 500 was >7.5% from its 3-month high.

Returns in terms of gains vs. losses following these occurrences were basically a toss-up across all time frames out to 6 months. The median returns, however, were considerably weaker than normal as were the drawdowns.

Does this study cinch an up-move in the market from here? Obviously not. The sample size is small and there are no guarantees in this business anyway. However, we will go back to our instinct. There certainly are legitimate concerns in the marketplace right now that may warrant having some hedges on. However, the extent of the fear being displayed by options traders seems disproportionate to the damage that has been inflicted in the market recently. That leads us to believe that these traders are perhaps getting spooked just a bit too easily.

_____________

More from Dana Lyons, JLFMI and My401kPro.

The commentary included in this blog is provided for informational purposes only. It does not constitute a recommendation to invest in any specific investment product or service. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.