S&P 500 & VIX Both Jump: Which One Will Blink?

While the S&P 500 closed at another new high, the VIX also spiked, an unusual occurrence that may have negative implications in the intermediate-term.

Among the themes in the stock market of late are the inexorable drift higher in the major averages and the rock-bottom levels to which the VIX has dropped, and stayed. On Wednesday, the former persisted but, in a stunning fashion, the latter did an about-face. Specifically, while the S&P 500 rose a half of one percent to another all-time high, the VIX, a.k.a., the S&P 500 Volatility Index, actually jumped by more than 11%. If you think that sounds odd, you’re actually underestimating the situation.

This was the largest rise in the VIX on a day in which the S&P 500 gained as much as .5% in 20 years, and just the 8th time it ever gained so much on such days since the VIX’s inception in 1986. It was also just the 8th time ever that the VIX jumped by as much as 11% when the S&P 500 hit a 52-week high – and also the first time in 20 years.

We took a closer look at that last statistic pertaining to the VIX’s behavior at S&P 500 new highs to try to ascertain any potential edge in the market’s subsequent behavior. As 7 precedents, and none in the last 20 years, hardly helps in examining the meaning behind this development, we have loosened the parameters a bit. Specifically, we looked at all days on which the S&P 500 closed at a 52-week high and the VIX rose by more than 4%.

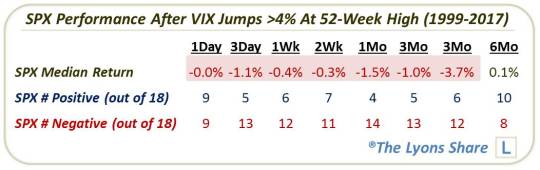

As it turns out, Wednesday’s occurrence makes the 19th such day since 1999.

From a glance at the chart, it may appear that many of the prior events occurred near short or intermediate-term tops. That observation would be correct. As such, the aggregate performance of the S&P 500 subsequent to the prior events was sub-par, particularly in the intermediate-term.

As the table shows, the median performance for the S&P 500 was negative from 1 day out to 3 months, with the 3-month figure actually being the weakest of all time frames. Returns were especially consistently negative in the intermediate-term time frames, with just 4 of the 18 events showing a positive 1-month return, and just 5 and 6 over 2 months and 3 months, respectively.

We will also mention that this odd dynamic occurred 37 times between 1986-1998. Why did we not include those occurrences? First, that earlier VIX regime behaved a little differently than in recent years. And we always place more weighting to occurrences in more recent periods. Additionally, and related, there was not much of a trend to the market’s behavior following those earlier events. The S&P 500′s returns were somewhat lackluster out several months, but not egregiously so.

What is the reason for this odd VIX behavior? We can’t say, nor are we typically interested in the “why”. Some have suggested it may be related to the expiration of VIX options. That may be the case, but history does not put asterisks next to historical data so we try not to rationalize things too much. Thus, taking this unusual circumstance at face value, we would have to say the odds favor the S&P 500 “blinking”, i.e., the VIX has the better forecasting record and better chance of being “right”.

That may be troublesome for stock investors over the next few weeks and months.

_____________

Like our charts and analysis? Get an all-access pass to our complete macro market assessment at our new site, The Lyons Share.

Disclaimer: JLFMI’s actual investment decisions are based on our proprietary models. The conclusions based on the study in this letter may or may not be consistent with JLFMI’s actual investment posture at any given time. Additionally, the commentary provided here is for informational purposes only and should not be taken as a recommendation to invest in any specific securities or according to any specific methodologies. Proper due diligence should be performed before investing in any investment vehicle. There is a risk of loss involved in all investments.